Underwriting & risk teams independent auto lending

The losses are already in the application. Your underwriters just can't see them yet.

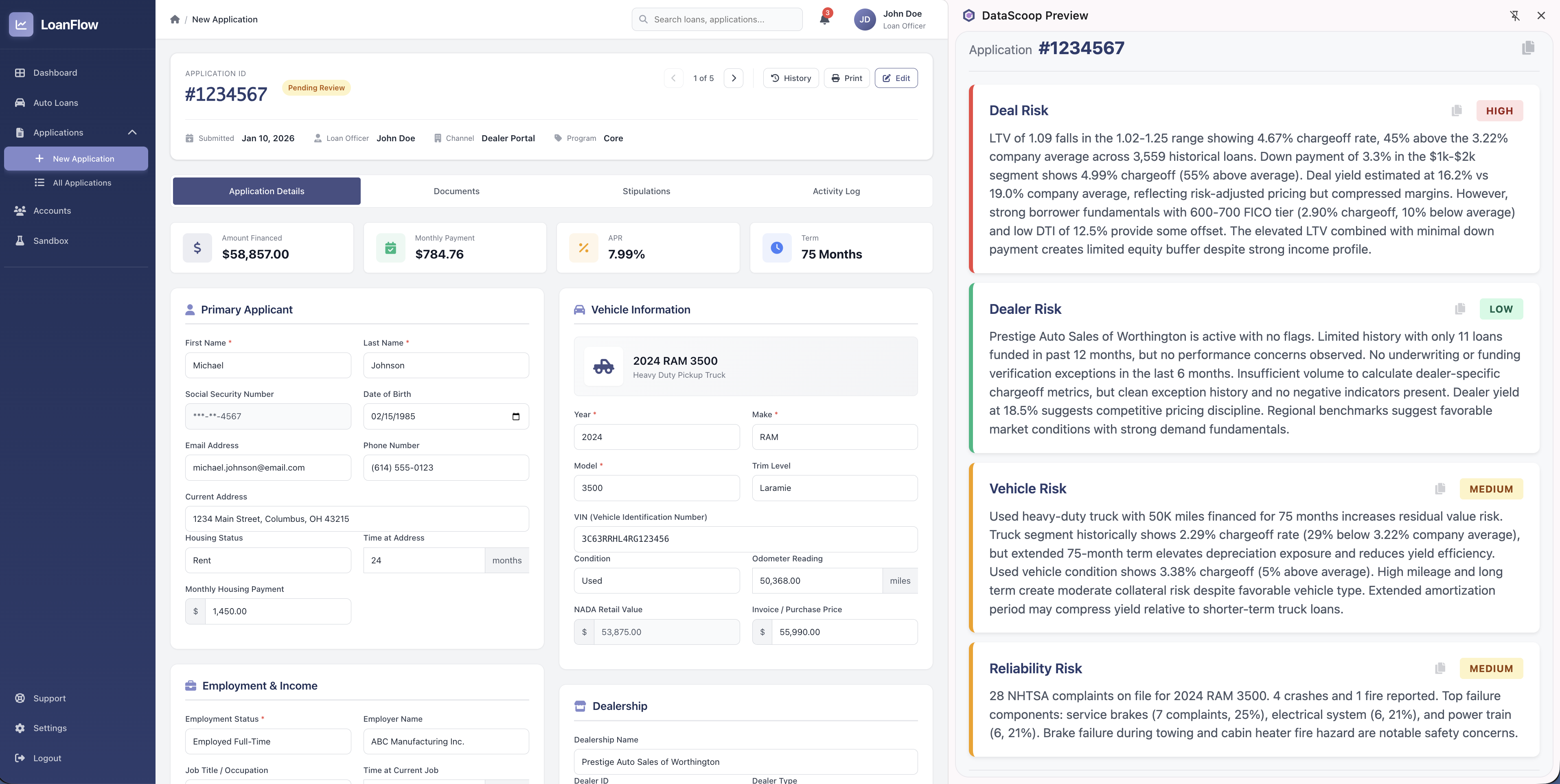

Every deal carries a dealer story, a collateral story, a deal-structure story. Sidecar puts all of it next to the application — deal, dealer, vehicle, and reliability risk, each read against your own loan history — the moment the decision gets made.

✓ 60-day money-back guarantee. Live in days, not quarters — no LOS integration.